Is a Career in Exercise Science Right For You? Take The Free Quiz

Lionel University courses and programs are 100% distance education with no residency requirement. Dormitory facilities, housing availability, and institutional assistance with housing is not offered and does not apply. All coursework is delivered through our online Learning Management System (LMS), accessible via secured username and password through lionel.edu. This course delivery platform is designed with an easy-to-use student interface. The LMS is used by students and faculty members for course syllabus, course work, and grading. Supported by the course instructor and the accompanying digital textbook, the LMS is the students’ online classroom.

Students may begin classroom orientation shortly after registration. It is recommended that students complete classroom orientation prior to starting their first course. The purpose of classroom orientation is to help the student navigate the LMS, understand the process for successfully completing a course, and utilize all helpful student resources.

The Family Educational Rights and Privacy Act of 1974 (FERPA) is a U.S. federal law that gives students access to their records and protects the privacy of their education records. Lionel University may not disclose personally identifiable information about students or allow inspection of their education records without written permission unless such action is covered by certain exceptions permitted by the act.

Once a student has registered for courses at Lionel University, all rights provided by FERPA rest with the student even if the student is younger than 18 years old. This applies regardless of country of residence or citizenship.

FERPA grants five basic rights to you as a student:

• To inspect and review the information maintained in your student record.

• To seek an amendment to your records and in certain cases add a statement to the record.

• To consent to disclosure of his/her records (with exceptions).

• To obtain a copy of the institution’s policy.

• To file a complaint with the Department of Education if Lionel University fails to comply with FERPA Policies.

Family Policy Compliance Office U.S. Department of Education

400 Maryland Avenue, SW.

Washington, DC 20202-4605

Directory Information

Directory Information may be released without written authorization. FERPA defines Directory Information as being information not generally considered harmful such as name, address, enrollment status, telephone, e-mail, place of birth, degree, and awards, etc.

Lionel University considers the following to be directory information:

• Student's name

• Address

• Telephone number

• E-mail address

• Date and place of birth

• Major field of study

• Enrollment status

• Dates of attendance and graduation

• Degrees, honors, and awards received

If you decide to request that your directory information not be disclosed, please send a request for a Directory Information Block via email to your Success Coach. The request must come from the email address specified in your student record and must include your student ID for us to process it.

Non-Directory Information

Non-Directory Information may only be released to third parties (including parents, spouses, and siblings) with written authorization. If a third-party tuition assistance agreement requires Lionel University to report grades or academic status, only the information required by the agreement will be reported (e.g., Military Tuition Assistance, VA benefits). Some examples of non-directory information are:

• Race, ethnicity, and citizenship

• Grades, GPA, course schedule

• Documents required for admission

• Billing or Financial Aid Information

Giving Access to a Third-Party

You may sign a Third-Party Authorization Form to allow FERPA protected information to be released to a third party. To request the form, email your Success Coach at support@lionel.edu. The request must come from the email address in your student record and must include your student ID for us to process it.

Background:

Lionel University is committed to achieving an alcohol- and drug-free workplace. Alcohol and other drug abuse is a significant public health problem and has a detrimental effect on the community in terms of increased medical and worker’s compensation claims, medical disability costs, decreased productivity, injuries, theft, and absenteeism. Accordingly, Lionel University has the right and obligation to maintain a safe, healthy, and productive working and learning environment and to protect Lionel University property, operations, and reputation.

Students, faculty, and staff must comply with the federal, state, and local laws concerning alcohol and illegal drug usage, whether on University property or otherwise. Violations will be reported to the appropriate law enforcement officials. Individuals will be subject to Lionel University disciplinary action, up to and including expulsion or separation, pursuant to the University’s policies and procedures. Our Administration reserves the right to impose one or more disciplinary actions, including successful completion of a substance abuse program as a condition to continue enrollment or employment, at the cost of the individual.

Enforcement Summary:

Based on our commitment to improve the quality of education, all individuals have a personal responsibility to encourage compliance with this policy.

Any employee—faculty member, student, staff member, or administrator—who does not abide by this statement is subject to:

Personal action up to and including termination or expulsion, or

Satisfactory participation in an educational, assistance, or rehabilitation program related to alcohol and drug abuse that is approved by a federal, state, local health, law enforcement, or other appropriate agency. The cost of the program will be paid by the individual if not covered by insurance.

The decision on the severity of action taken will depend, in part, upon the nature of the offense, the sensitivity of the position held, and the outcome of participation in the program described above.

Employees or students who are not terminated or expelled may also be referred to appropriate self-help groups.

Students in violation of the laws regulating alcohol and controlled substances or Lionel University policies concerning alcohol and drugs may receive, in addition to criminal sanctions, Lionel University sanctions including, but not limited to, the following: fines, education programming, probation, or dismissal.

Employees of Lionel University found in violation of laws regulating alcohol or controlled substances, may receive, in addition to criminal sanctions, Lionel University sanctions including: official reprimand, suspension, or termination. Employees in violation will be subject to disciplinary action as outlined in their respective employee handbooks.

Education Summary:

All employees receive an annual email that contains the details and ramifications of violating Lionel University's drug and alcohol policy. New employees are provided the information within the first three months of their employment. The drug and alcohol awareness information includes:

The content of this policy.

The extent and nature of the abuse problem, including national and Lionel University statistics, as well as social, personal, and health risks.

Recognition of symptoms of abuse and discussion of recent perspectives on the problems (i.e., focus on prevention, environment, and norms rather than only on full-blown addiction, value of early intervention, process of addiction, and health risks).

Referral information on available counseling, rehabilitation, and self-help groups.

Penalties to be imposed for violation of this policy.

Assessment Summary:

Assessment activities to guide program development will be conducted by the Administration and results will be used to evaluate and guide program development. Assessment, at a minimum, will include the following information:

An appraisal of the environment for subtle causes of alcohol and drug abuse;

The collection and use of summary health and counseling client information;

The collection and use of summary data from drug-related disciplinary actions.

Notification to Faculty Staff and Students

This letter is sent electronically on an annual basis.

*******************************************************************

Dear Students and Faculty,

As a Federal requirement for higher education institutions, Lionel University is sending an annual notification to students and faculty members per the Drug-Free Schools and Communities Act (DFSCA) and Drug and Alcohol Prevention Regulations.

It is Lionel University’s position that no student or faculty member should use drugs or alcohol while attending class or while on Lionel University’s campus. Lionel University does not condone the use of any illegal drug or alcohol whatsoever for any student or faculty member.

Please review the following information pertaining to drugs and alcohol while attending Lionel University.

Sanctions

Students in violation of the laws regulating alcohol and controlled substances or University policies concerning alcohol and drugs may receive, in addition to criminal sanctions, University sanctions including, but not limited to, the following: fines, education programming, probation, or dismissal. Students in violation will be subject to judicial system policies and procedures as outlined.

Employees of Lionel University found in violation of laws regulating alcohol or controlled substances or University policies concerning these substances, may receive, in addition to criminal sanctions, University sanctions including official reprimand, suspension, or termination. Employees in violation will be subject to disciplinary action as outlined.

Any student facing a drug-related conviction may not qualify for federal aid.

Health Risks Associated with Drugs and Alcohol

There are multiple health risks associated with drugs and alcohol, and these substances can affect various parts of the body, including liver, muscles and bones, nose, lungs, stomach, brain, heart, pancreas and intestines, sex organs, immune systems, and blood vessels.

Counseling, Treatment, and Rehabilitation

Lionel University will provide information about local counseling, treatment, and rehabilitation for students or faculty members when needed based on the student’s need. Please contact the school for information.

End of Letter:

*******************************************************************

Detailed Policy on Alcohol and Drug Abuse Prevention

To comply with federal regulations, Lionel University is required to send an annual notification to students and faculty members per the Drug-Free Schools and Communities Act (DFSCA) and Drug and Alcohol Prevention Regulations.

As required by law, Lionel University administration will also conduct an annual review of its program to (a) determine its effectiveness and implement changes if needed and (b) ensure that the sanctions developed are consistently enforced. This annual meeting is part of the Compliance Committee’s annual meeting held during the first quarter of each year.

It is our intent and obligation to provide a drug and alcohol-free, healthy, safe, and secure working and learning environment. Staff, faculty, and students are expected and required to adhere to this policy. Staff, faculty, and students are not permitted on the premises if under the influence of drugs or alcohol.

In addition to the aforementioned requirement, all staff, faculty, and students will adhere to the following:

The unlawful manufacture distribution, possession, dispensing, or use of a controlled substance on company premises or while conducting company business off campus is absolutely prohibited. Violations of this policy will result in disciplinary action, up to and including termination of employment, dismissal of the student, and may include legal consequences as allowed by federal, state, and local laws.

We recognize drug and alcohol dependency as an illness and a major health problem. We also recognize drug and alcohol abuse as a potential health, safety, and security problem. Employees and students needing help in dealing with such problems may contact the Human Resources Department to obtain a listing of centers specializing in drug and alcohol counseling and rehabilitation. Lionel University will make every appropriate effort to assist a member of the staff, faculty, or student body.

Employees must, as a condition of employment, abide by the terms of the above policy and report any conviction under a criminal drug or alcohol statute for violations occurring on or off company premises while conducting business. A report of a conviction must be made to the Director of Accounting/Finance within five days after the conviction. (This requirement is mandated by the Drug-Free Workplace Act of 1988.)

Students suspected of engaging in drug or alcohol abuse on campus or in classes may be removed from class and possibly expelled. Lionel University has the right to request a drug or alcohol test from a student as part of our pledge to assist a student in rehabilitation and to remain as a student in the University.

An employee of the institution may be required to submit to a drug and/or alcohol test at any time. Refusal to consent to such testing established by the company shall be considered to constitute that employee’s resignation for personal reasons. An employee who tests positive will be subject to immediate termination at the sole discretion of the company administrators.

Any student, faculty, or member of the staff may be reported to local authorities if any parts of this policy are violated. Lionel University may also require certain rehabilitation be completed before a faculty, staff, or student may return to the University.

Lionel University promotes an alcohol-free workplace at all times.

All faculty and staff members are required to acknowledge Lionel University’s drug and alcohol-free policy upon employment.

Summary of Sanctions

It is the intent of Lionel University to institute fair and effective sanctions against persons who violate this policy which may also result in a violation of federal, state, or local laws.

Students in violation of the laws regulating alcohol and controlled substances or company policies concerning alcohol and drugs may receive, in addition to criminal sanctions, company sanctions including, but not limited to, the following: fines, educational programs on substance abuse, probation, or dismissal. Students in violation will be subject to judicial system policies and procedures as outlined.

If Lionel University suspects a student may be abusing a substance such as illegal drugs, alcohol, or prescription drugs, the student may be asked to leave the premises or class. Lionel University has the right to notify the local authorities.

Lionel University may require satisfactory participation in an educational, assistance, or rehabilitation program related to alcohol and drug abuse that is approved by a federal, state, local health, law enforcement, or other appropriate agency.

Employees of Lionel University found in violation of laws regulating alcohol or controlled substances or University policies concerning these substances, may receive, in addition to criminal sanctions, company sanctions including official reprimand, suspension, or termination. Employees in violation will be subject to disciplinary action as outlined.

The severity of the action taken by the company will depend, in part, upon the nature of the offense, the sensitivity of the position held for faculty and staff, time to graduation for students, the decision of the appeal committee, and the outcome of an approved substance abuse program as outlined above.

Faculty, staff, and students not expelled may also be referred to appropriate self-help groups.

Summary of Laws in California related to Alcohol and Drugs

Alcohol Laws

1) Persons under 21 years of age are prohibited from purchasing, attempting to purchase, or possessing intoxicating liquor.

2) It is a crime for those licensed to sell alcoholic beverages to sell or otherwise supply intoxicating liquor to persons under 21 years of age.

3) California prohibits selling or supplying intoxicating liquor to persons who appear to be intoxicated.

4) A person commits the crime of driving while intoxicated (DUI) if that person operates a motor vehicle while in an intoxicated or drugged condition. In California, a driver with eight-hundredths of one percent (.08 percent) of alcohol by weight in his or her blood is guilty of DUI and is presumed to be intoxicated without further evidence as to how the driver’s motor skills or operation of the automobile have been affected.

5) A person under 21 years of age may be charged with zero tolerance if he or she has one-hundredth of one percent (.01 percent) or higher of alcohol is his or her system when operating a motor vehicle.

6) Penalties for violation of California’s alcohol laws or alcohol-related traffic laws can include admin per se license suspension, criminal license suspension, fines, jail time or community service, DUI school, installation of ignition interlock device (IID), sr-22 filing and loss of driving privileges.

Drug Laws

1) All manufacture, sale, use, or possession of controlled or imitation of controlled substances violations are felonies with these exceptions:

titPossession of 28.5 grams or less of marijuana is an infraction, punishable by a fine of up to $100. (Ca. Health & Safety Code § 11357(b).)

Possession of more than 28.5 grams of marijuana is punishable by a fine of up to $500, up to six months in jail, or both. (Ca. Health & Safety Code § 11357(c).

Penalties include fines, probation, and jail terms. A student may lose eligibility for Title IV funds if convicted of a drug-related charge while using Title IV funds.

Summary of how the company may collect information about Drugs or Alcohol

1) A member of the faculty may observe a student behaving out of character or discussing drugs in class and disrupting class.

2) Anonymous tips from a credible source.

3) Directly from the person in question.

4) Students reporting odd behavior.

5) Using security cameras on campus.

6) Background checks before hiring faculty and staff.

7) Professional and character references.

Health Risks Associated with Drugs and Alcohol

There are multiple health risks associated with drugs and alcohol, and these substances can affect various parts of the body, including liver, muscles and bones, nose, lungs, stomach, brain, heart, pancreas and intestines, sex organs, immune systems, and blood vessels. Alcohol and drug use can also impair one’s ability to absorb and retain information and cause long-term brain damage.

For more information on how drugs and alcohol affect the body and how to avoid them, please view this free resource: http://www.drugfreeworld.org.

Common symptoms of substance abuse include but are not limited to the following:

*Odor of alcohol on the breath

*Unexplained changes in personal or professional relationships

*Deteriorating work performance

*Mood swings, increased anxiety, depression

*Unusual scarring or bruising

*Deterioration in appearance

*Social isolation

*Increased irritability

*speech, coordination, memory problems

*eye redness, irritation

Counseling, Treatment, and Rehabilitation

Lionel University will provide information about local counseling, treatment, and rehabilitation for students or faculty members based on the student’s need. Please contact any member of Lionel University staff to reach out for assistance. A qualified member of Lionel University staff will assist you with locating help.

Treatment of Substance Abuse Problems--Where To Go For Help

Lionel University believes that the most effective responses to instances of substance abuse rely on appropriate identification of the problem and the availability of effective, confidential assistance. Individuals with substance abuse problems are encouraged to seek such assistance and appropriate treatment options. The company also encourages members of the community to care about each other and to express concern for and to offer help to those engaged in substance abuse.

Faculty can provide individuals with advice about company policies and procedures, and the appropriate off-campus services.

Medical and Rehabilitation Leaves

Generally, the company provides rehabilitation leave to faculty and staff seeking treatment for drug or alcohol abuse. The company will make reasonable efforts to keep the basis of medical and rehabilitation leaves confidential.

Students seeking a medical leave and who plan to return may submit a written request for a leave of absence (LOA). The request must include the reason for leave and date of return. A Leave of Absence cannot exceed 180 days.

Students on an approved LOA are not considered withdrawn. Students seeking a medical leave should send a written request to the Student Affairs Committee (studentaffairs@lionel.edu). A physician or mental health professional must provide a written recommendation for the medical leave. Readmission for students on medical leave is contingent on a physician's or mental health professional's written recommendation. The Student Affairs Committee must approve the petition to return from a medical leave. A medical leave can be taken at any point in the quarter.

Faculty/staff members seeking a rehabilitation leave should contact the Chief Academic Officer. Any faculty or staff member who acknowledges a problem with drugs or alcohol, and who decides voluntarily to enroll in a rehabilitation program, may be granted a reasonable accommodation. This accommodation may include time off without pay and/or an adjusted work schedule provided the accommodation does not impose an undue hardship on the institution.

The costs of participation will be paid by the faculty member or the faculty member's health insurance provider.

Off-Campus Resources

The following resources may be helpful to individuals with substance abuse problems:

Alcoholics Anonymous (805) 962-3332

Al-Anon (805) 899-8302

Cocaine Anonymous (805) 969-5178

Narcotics Anonymous (805) 569-1288

Substance Abuse And Mental Health Services Administration (800) 662-4357

The following resources may be helpful to people who are in a relationship with an individual with a substance abuse problem or who grew up in a drug or alcohol affected, or other types of dysfunctional homes.

Adult Children of Alcoholics 1-800-331-0503

Co-Dependents Anonymous (888) 444-2359

Al-Anon (805) 899-8302

Summary of federal laws and policy that support a drug-free and alcohol-free campus

1) Pell Grant and Guaranteed Student Loans effective July 1987

2) The Drug-Free Workplace Act, effective March 1989

3) The Drug-Free Schools and Community Act Amendments, effective October 1990

Summary of this policy

1) No student, faculty, or staff member should be in possession of, use, or distribute drugs and alcohol on campus or at any institutional activities.

2) Applicable legal sanctions under local, state, and federal law for unlawful possession, use, or distribution of alcohol or controlled substances are clearly outlined and available to view in the annual distribution of this information.

3) A description of the health risks associated with drug and alcohol use.

4) Referral and treatment information.

5) A clear statement of disciplinary actions that the University will impose on students and employees who may violate this policy.

Financial Student Aid

LOSS OF AID ELIGIBILITY ASSOCIATED WITH DRUG-RELATED OFFENSES AND HOW TO REGAIN ELIGIBILITY (as taken directly from Volume 1 of the Student Financial Aid Handbook).

The chart below illustrates the period of ineligibility for FSA funds, depending on whether the conviction was for sale or possession and whether the student had previous offenses. (A conviction for sale of drugs includes convictions for conspiring to sell drugs.)

Possession of Illegal Drugs

1st Offense - 1 year from date of conviction

2nd Offense - 2 years from date of conviction

3+ Offenses - Indefinite period

Sale of Illegal Drugs

1st Offense - 2 years from date of conviction

2nd Offense - Indefinite period

3+ Offenses - Indefinite period

If the student was convicted of both possessing and selling illegal drugs, and the periods of ineligibility are different, the student will be ineligible for the longer period.

Schools must provide each student who becomes ineligible for Title IV aid due to a drug conviction a clear and conspicuous written notice of his loss of eligibility and the methods whereby he can become eligible again.

A student regains eligibility the day after the period of ineligibility ends or when he successfully completes a qualified drug rehabilitation program or, effective beginning with the 2010–2011 award year, passes two unannounced drug tests given by such a program. Further drug convictions will make him ineligible again.

Students denied eligibility for an indefinite period can regain it after successfully completing a rehabilitation program (as described below), passing two unannounced drug tests from such a program, or if a conviction is reversed, set aside, or removed from the student’s record so that fewer than two convictions for sale or three convictions for possession remain on the record. In such cases, the nature and dates of the remaining convictions will determine when the student regains eligibility. It is the student’s responsibility to certify to you that she has successfully completed the rehabilitation program; as with the conviction question on the FAFSA, you are not required to confirm the reported information unless you have conflicting information.

When a student regains eligibility during the award year, you may award Pell, ACG, National SMART, TEACH, and Campus-based aid for the current payment period and Direct and FFEL loans for the period of enrollment.

Standards for a Qualified Drug Rehabilitation Program

A qualified drug rehabilitation program must include at least two unannounced drug tests and must satisfy at least one of the following requirements:

Be qualified to receive funds directly or indirectly from a federal, state, or local government program.

Be qualified to receive payment directly or indirectly from a federally or state-licensed insurance company.

Be administered or recognized by a federal, state, or local government agency or court.

Be administered or recognized by a federally or state-licensed hospital, health clinic, or medical doctor.

If you are counseling a student who will need to enter such a program, be sure to advise the student of these requirements. If a student certifies that he has successfully completed a drug rehabilitation program, but you have reason to believe that the program does not meet the requirements, you must find out if it does before paying the student any FSA funds.

Drug Convictions

HEA Section 484(r)

34 CFR 668.40

Drug Abuse Hold

The Anti-Drug Abuse Act of 1988 includes provisions that authorize federal and state judges to deny certain federal benefits, including student aid, to persons convicted of drug trafficking or possession. The CPS maintains a hold file of those who have received such a judgment, and it checks applicants against that file to determine if they should be denied aid. This is separate from the check for a drug conviction via question 23; confirmation of a student in the drug abuse hold file will produce a rejected application and a separate comment from those associated with responses to question 23. See the ISIR Guide for more information. 1–16 Vol. 1—Student Eligibility 2010–11 FSA HB JUL 2010

End of Policy.

(Last updated March of 2023)

University transfer credits are determined by the receiving institution. Each institution is responsible for determining its own policies and practices with regard to the transfer and award of credit. It is the receiving institution’s responsibility to provide reasonable and definitive policies and procedures for determining a student’s knowledge in required subject areas. Lionel University will furnish transcripts and other documents necessary for a receiving institution to judge the quality and quantity of the work completed by its students. Be advised that the work reflected on the transcript may or may not be accepted by a receiving institution.

Transfer Credit

Credit transfer depends on:

Accreditation: Accreditation speaks primarily to the first of these considerations, serving as the basic indicator that an institution meets certain minimum standards. Lionel University gives careful attention to the accreditation conferred by accrediting bodies recognized by the Council for Higher Education Accreditation (CHEA and/or the U.S. Department of Education (USDE). CHEA is a non-profit organization of colleges and universities that has a formal process of recognition that requires recognized accrediting bodies to meet the same, generally accepted minimum standards for accreditation. USDE has a governmental process of recognition that requires recognized accrediting bodies to meet federal standards ensuring that education provided by accredited institutions of higher education meets acceptable levels of quality.

Comparability and Applicability: Comparability of the nature, content, and level of transfer credit and the appropriateness and applicability of the credit earned in programs offered by the receiving institution are important in the evaluation process. This information is obtained from catalogs and other materials and from direct contact between staff at both the receiving and sending institutions.

Admissions and Degree Purposes: There may be differences between the acceptance of credit for admission purposes and the applicability of credit for degree purposes. A receiving institution may accept previous work, place a credit value on it, and enter it on the transcript. However, that previous work, because of its nature and not its inherent quality, may be determined to have no applicability to a specific degree to be pursued by the student.

Unaccredited Institutions: Institutions of postsecondary education that are not accredited by CHEA-recognized accrediting bodies may lack that status for reasons unrelated to questions of quality. Such institutions, however, cannot provide a reliable, third-party assurance that they meet or exceed minimum standards. That being the case, students transferring from such institutions may encounter special problems in gaining admission and in transferring credits to accredited institutions.

Foreign Institutions: In most cases, foreign institutions are chartered and authorized by their national governments, usually through a ministry of education. Although this provides for standardization within a country, it does not produce useful information about comparability from one country to another. The Council on International Education Exchange, Council on Evaluation of Foreign Credentials, National Liaison Committee on Foreign Student Admissions, and National Association of Foreign Student Affairs can assist with information or guidelines on admission and course placement of foreign students. Equivalency or placement recommendations are evaluated in terms of programs and policies of the individual receiving institution.

Validation of Extra-Institutional and Experiential Learning for Transfer Purposes: Transfer-of-credit policies encompass educational accomplishment attained in extra-institutional settings as well as at accredited postsecondary institutions. Recommendations provided by the American Council on Education’s Office, credit-by-examination programs, and the Council for Adult and Experiential Learning help to determine credit equivalencies for various modes of extra-institutional learning.

Lionel University accepts previous general education and elective coursework from an institution that is (or was at the time the course was completed) accredited by an organization recognized by either the U.S. Department of Education or CHEA. Transfer credit is only applied to degree programs and is not accepted for certificate completion.

Transferable coursework from outside institutions must be:

Here are the types of credit accepted:

Please Note: Lionel University’s school code for the CLEP examination is: 4898.

Credit earned in repeatable required courses may be applied only once to the degree requirements.

Some study abroad programs, upon approval, may satisfy some general education and/or elective requirements.

Relevant experiential learning as gained through the military and evaluated by the American Council on Education (ACE) for undergraduate credit can satisfy some general education or elective requirements. Official military transcripts are required. This institution does not award credit for any other prior experiential learning.

Credit awarded for experiential or equivalent learning, including credit-by-examination, cannot exceed 25 percent of the credits required for the degree.

Articulation Agreements

Lionel University holds articulation agreements with:

Huntington University of Health Sciences

Lionel University students who transfer to Huntington University of Health Sciences have their coursework evaluated on a course-by-course basis to determine which of the Huntington University of Health Sciences general education requirements and discipline requirements have been met. Graduates of Lionel University’s AS in Exercise Science program will qualify for junior year standing upon admission to the Huntington University of Health Sciences BS in Nutrition program.

American College of Healthcare Sciences USA (ACHS)

ACHS accepts Lionel University certificate courses (PTR) with a grade of B or higher for transfer credit. The student must successfully complete all admission requirements and enroll as a new student at ACHS within five years following completion at Lionel University to receive transfer credit under this agreement. Upon enrolling at ACHS and submitting official Lionel University transcripts, the ACHS Registrar will note the appropriate award of credit to the student’s transcript without additional charge. This credit will be recorded as “Transfer Credit” on the academic transcript and will be excluded when calculating the student’s grade point average. There will be no cost to the student for Transfer Credit obtained in this manner. Please be aware that the administrative fee structure at ACHS is subject to change.

United States Sports Academy (USSA)

USSA will admit qualified students from Lionel University associate’s degree program

into its Bachelor of Sports Science Degree Program. USSA will also admit qualified students from Lionel University into its Master of Sports Science in Sports Exercise Science program. The Bachelor degree program offers majors in Sports Coaching, Sports Management, Sports Strength and Conditioning, and Sports Studies. Admission fee will be waived for any student graduating with an AS degree from Lionel University.

Articulation agreements are subject to change. Confirm the terms of these agreements with the articulating institution before you enroll.

Transfer Credit Evaluation

A completed program application and official transcripts from the conferring institution are required to facilitate credit evaluation. Transcripts for comparable Lionel University undergraduate courses completed in a country other than the United States must be evaluated by an outside credential evaluation company before they are submitted to Lionel University. The National Association of Credential Evaluation Services (www.naces.org) members are acceptable sources for foreign credential evaluation and translation services. Transcripts in languages other than English must be accompanied by a certified translation.

Credit for experiential learning from NCCA-accredited personal training courses or ISSA courses is awarded upon successful passing of corresponding competency exams with a score of 75% or higher (BS program: maximum of 4, AS program: maximum of 2; Master Trainer certificate: maximum of 1). Competency exams must be completed within the students first term in Lionel University. Applicants must submit proof of certification to registrar@lionel.edu. (Note: Transferred certification courses do not result in an ISSA certification.)

Lionel University operates on a quarter system and courses are awarded quarter credit. If a student transfers over credit taken at a semester based institution, the credit is converted to the quarter equivalent. One quarter credit is equivalent to two-thirds of a semester credit.

Any course or credit recommendation (institutional or non-institutional) approved to transfer to Lionel University degree requirements is evaluated on the quarter credit worth in addition to standards of educational quality to determine the applicability to Lionel University degree requirements.

Credits applied towards degree requirements are recognized only for the quarter credit required for that specific degree requirement. No additional credit will be awarded beyond the quarter credits required.

The prospective student must provide the following documentation:

Once the Transfer Credit Evaluation is complete, accepted transfer credit is applied to the degree plan and supplied to the applicant. The institution will maintain a written record of an applicant’s previous education and training, the record will clearly indicate that credit has been granted if appropriate, and the degree requirements will be shortened accordingly. To appeal the results of a transfer credit evaluation, contact the Office of the Registrar.

Competency Exam Policy

Relevant experiential learning from NCCA-accredited personal training courses within the Fitness and Wellness industry (including ISSA LLC) can be transferred in to satisfy core or elective credit in Lionel University degree programs. Credit will be awarded upon successful passing of a competency exam with a 75%. All competency exams must be completed within the students first term in Lionel University. If an exam is not completed in the first term, a $15 fee will be charged to the student in order to take the exam. Students are allowed two attempts to pass the exam. After two unsuccessful attempts, transfer credit will not be awarded.

NOTICE CONCERNING TRANSFERABILITY OF CREDITS AND CREDENTIALS EARNED AT OUR INSTITUTION

The transferability of credits you earn at Lionel University is at the complete discretion of an institution to which you may seek to transfer. Acceptance of the (degree, diploma, or certificate) you earn in the educational program is also at the complete discretion of the institution to which you may seek to transfer. If the (credits or degree, diploma, or certificate) that you earn at this institution are not accepted at the institution to which you seek to transfer, you may be required to repeat some or all of your coursework at that institution. For this reason you should make certain that your attendance at this institution will meet your educational goals. This may include contacting an institution to which you may seek to transfer after attending Lionel University to determine if your (credits or degree, diploma, or certificate) will transfer.

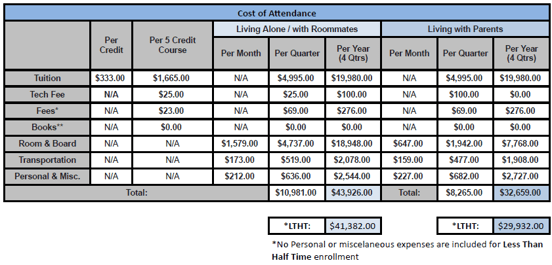

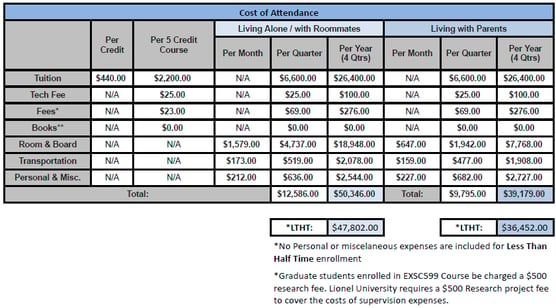

Tuition is due on a quarterly basis. Based on the tuition rate of $333 per credit, quarterly tuition for a full-time student enrolled in 15 credits is $4,995. The estimated total annual expense is $14,985 (45 quarter credits completed per year). The estimated total tuition and fees for the FSA eligible programs funds are:

Master Trainer Certificate

30 quarter credits + Fees

$11,394

Associate of Science in Exercise Science with an Emphasis in Personal Training

90 quarter credits + Fees

$31,769

Bachelor of Science in Exercise Science

180 quarter credits + Fees

$62,254

Master of Science in Exercise Science

45 quarter credits + Fees

$20,055

Estimates based on tuition rate of $333 per credit hour and a $22.50 proctor fee for each course taken. Number of credits and courses take for a degree programs can vary by electives chosen.

Before applying for financial aid, students and parents should assess all the costs associated with attending Lionel University. The Financial Aid office establishes standard budgets, which reflect standard costs for students during a typical quarter of enrollment. Actual expenses vary among students depending upon lifestyles, priorities, and obligations.

Undergraduate

Graduate

Refunds, if applicable and requested, will be made within 30 days of request via the original payment method.

If cancellation occurs at any time within 7 calendar days after the institution accepts enrollment, the student may request a refund of all money paid to the institution.

Undergraduate and graduate courses:

Self-paced certificate courses:

Students who have received federal student aid funds and cancel up through the 60% point are entitled to a refund of moneys not paid from federal student aid program funds, if applicable.

Iowa students are entitled to a 100% refund of tuition through the first day of class.

Iowa students who withdraw before the final day of class will receive a prorated refund, calculated by multiplying the amount of tuition the student was charged by a ratio of the number of calendar days remaining/incomplete in the term as of the withdrawal date, as compared to the total calendar days in the term.

Lionel University accepts cancellation in any manner. However, California state statutes require that students verify cancellation in writing. Therefore, please supplement any verbal requests with written notice within 30 days. Written notice can be in any form including email (registrar@lionel.edu) or mail (1015 Mark Ave, Ste 1013, Carpinteria, CA 93013).

The institution reserves the right to cancel a student’s enrollment for violations of student conduct, including, but not limited to, a student’s lack of attendance.

Undergraduate courses:

Total course length in days Total tuition ÷ Number of days completed in the course

Refund Policy Example – Student Paid $3,996 total tuition # Days 31 / 70 = 44% $3,996 * (1 - 0.44) = $2,237.76 net refundable tuition

Refund Policy Example – Student Responsibility $3,996 total tuition # Days 31 / 70 = 44% $3,996 * 0.44 = $1,758.24 net student responsibility = Refund amount

This is an example only. Student finances are individualized and vary from student to student.

Graduate courses:

Total tuition ÷ Total course length in days = Refund amount Number of days completed in the course

Refund Policy Example – Student Paid $2200 total tuition # Days 31 / 70 = 44% $2200 * (1 - 0.44) = $1232 net refundable tuition

Refund Policy Example – Student Responsibility $2200 total tuition # Days 31 / 70 = 44% $2200 * 0.44 = $968 net student responsibility

This is an example only. Student finances are individualized and vary from student to student.

Self-paced certificate courses:

Total number of course assignments Course cost ÷ Number of course assignments completed Course cost– Refund amount + $25 (S&H) Total amount student is responsible for paying

Refund Policy Example – Student Paid $675 total tuition # Assignments 4 / 10 = 40% $675 * (1 - 0.40) = $405 net refundable tuition

Refund Policy Example – Student Responsibility $675 total tuition # Assignments 4 / 10 = 40% $675 * 0.40 = $270 net student responsibility = Refundable tuition

This is an example only. Student finances are individualized and vary from student to student.

Return of Title IV (R2T4)

Title IV funds are awarded to a Lionel University student under the assumption that the student will attend school for the entire period for which the assistance is awarded. When a student withdraws, ceases to attend, is dismissed, or fails to return from an approved leave of absence, the institution will determine the amount of aid the student earned. This will determine any Title IV aid that must be returned to the US Department of Education or disbursed to the student as a post-withdrawal disbursement.

The calculation is based on the number of days completed by the Last Date of Attendance (LDA) or official withdrawal notice, divided by the total days the student was scheduled to attend during the quarter at the time the student ceased attendance in all courses.

Up through the 60% point in the student’s scheduled enrollment, the earned amount of Title IV funds is prorated through the withdrawal date or LDA. After the 60% point, the student will earn 100% of the Title IV funds disbursed for their scheduled enrollment. Any unearned portion of FSA funds that were disbursed must be returned to their respective programs. Lionel University will return any FSA funds used to pay institutional charges as determined by the R2T4 calculation. The student may be required to return unearned grant funds to the Department of Education via direct payments, or Direct Loan funds via the terms of the Master Promissory Note. A student may receive a post-withdrawal disbursement if the student earned more federal financial aid than was disbursed. The institution will return funds or offer to issue post-withdrawal disbursements of Direct Loan funds within 45 days of the date it determined the student withdrew.

The student is responsible for repaying the institution for any balance on their account resulting from the institution returning FSA funds originally used to cover tuition and fees on the student’s behalf. After any FSA funds have been returned, the student’s balance will be displayed under the Financial tab of the student portal. Failure to pay the balance in full will result in a financial hold being placed on the student’s account. Students on financial hold are not permitted to register for classes (or, in some cases, remain registered in class).

If the student does not repay grant funds that are owed to the US Department of Education within 45 days of being notified, the account will be turned over to the Department as an overpayment. Students who owe an overpayment of Title IV funds are ineligible for further disbursements of FSA funds at any institution until the overpayment is paid in full or satisfactory payment arrangements have been made with the Department.

Order of Refund

Refunds are allocated in the following order:

Students are asked to discuss dropping a course with their Success Coach. A student may drop a course without receiving a “W” if they drop by the last day of the first week of class. The final withdrawal deadline is the end of the 3rd week in a 5-week course and the end of the 6th week in a 10-week course. Students who officially withdraw from a course before the final withdrawal deadline will receive a “W.” Beyond the final withdrawal deadline, grades will be calculated as points earned, divided by the total course points. All deadlines are in the institution’s time zone.

The refund procedure and schedule described above shall apply to all drops and withdrawals. For veteran students, the VA Office will be notified of all dropped courses or withdrawals

Official Withdrawal: Students can request withdrawal from the school in any manner. California state statutes require that students verify cancellation in writing. Therefore, please supplement any verbal requests with written notice within 30 days. Written notice can be in any form including email (billing@lionel.edu) or mail (1013 Mark Ave, Carpinteria, CA 93013).

Unofficial Withdrawal: Students who cease attendance and do not provide official notification of their intent to continue in their classes may be considered for administrative withdrawal.

Lionel University does not discriminate on the basis of disability. Lionel University has adopted an internal grievance procedure providing for prompt and equitable resolution of complaints alleging any action prohibited by Section 504 of the Rehabilitation Act of 1973 (29 U.S.C. 794).

Lionel University does not discriminate in admission or access to our program on the basis of age, race, color, sex, disability, religion, sexual orientation, national origin or any other category protected by local, state or federal laws. Applicants who are persons with disabilities, as defined in paragraph 104.3(j) of the regulation under Section 504 of the Rehabilitation Act of 1973, may apply for admittance into the program. Lionel University will work with the applicant or student to determine whether reasonable accommodations can be effective and/or are available.

Lionel University's ADA Compliance Coordinator: Kelly Bonice| kbonice@lionel.edu | 800-650-4772 is responsible for coordinating compliance with Section 504 of the Rehabilitation Act of 1973 and Title III of the Americans with Disabilities Act of 1990.

Request for Accommodation

If you would like to request academic adjustment or auxiliary aids, please contact your Academic Advisor. You may request academic adjustments or auxiliary aids at any time.

Any qualified individual with a disability requesting an accommodation or auxiliary aid or service should follow this procedure:

1) Notify your Academic Advisor in writing of the type of accommodation needed, date needed, documentation of the nature and extent of the disability, and of the need for the accommodation or auxiliary aid. The request should be made at least four weeks in advance of the date needed.

Email: support@lionel.edu

2) Your Academic Advisor will respond within two weeks of receiving the request.

3) If you would like to request reconsideration of the decision regarding your request, please contact your Academic Advisor within one week of the date of the response. Please provide a statement of why and how you think the response should be modified.

Section 504 Internal Grievance Procedure

Section 504 prohibits discrimination on the basis of disability in any program or activity receiving Federal financial assistance. The Law and Regulations may be examined in the office of Kelly Bonice who has been designated to coordinate the efforts of Lionel University to comply with Section 504. The Compliance Coordinator can be contacted by phone number at 1-805-364-0612 or by email at kbonice@lionel.edu.

Any person who believes she/he has been subjected to discrimination on the basis of disability may file a grievance pursuant to the procedure outlined below. Lionel University will not retaliate against anyone who files a grievance in good faith or cooperates in the investigation of a grievance.

Procedure:

Grievances must be submitted to Kelly Bonice, 1-805-364-0612 or by email at kbonice@lionel.edu the Section 504 Grievance Compliance Coordinator, within thirty (30) days of the date, the person filing the grievance becomes aware of the alleged discriminatory action.

A complaint must be in writing, containing the name and address of the person filing it. The complaint must state the problem or action alleged to be discriminatory and the remedy or relief sought.

The Section 504 Grievance Compliance Coordinator (or his designee) shall investigate the complaint (i.e., identify and obtain relevant evidence, identify and obtain statements from relevant witnesses) and afford all interested persons an opportunity to submit relevant evidence. The Complainant may also present witnesses relative to the complaint. The Section 504 Grievance Compliance Coordinator will maintain the files and records relating to such grievances. The Section 504 Grievance Compliance Coordinator will issue a written decision on the grievance no later than 30 days after its filing.

The person filing the grievance may appeal the decision of the Section 504 Grievance Compliance Coordinator by writing to Lionel University’s Executive Director, Dr. Salvatore A. Arria, 1013 Mark Avenue, Carpinteria, CA 93013 who can be reached at 800-650-4772 or by email at sarria@lionel.edu within 15 days of receiving the Section 504 Grievance Coordinator’s decision. The Executive Director shall issue a written decision in response to the appeal no later than 30 days after its filing.

The availability and use of this grievance procedure does not prevent a person from filing a complaint of discrimination on the basis of disability with the U. S. Department of Education, Office for Civil Rights.

Lionel University will take all steps to prevent recurrence of any harassment or other discrimination and to correct discriminatory effects where appropriate. Lionel University will make appropriate arrangements to ensure that disabled persons are provided other accommodations, if needed, to participate in this grievance process. The Section 504 Compliance Coordinator will be responsible for such arrangements.

Course enrollees agree that all Information within the institution's courses, course texts, accompanying workbooks, and websites, etc. are protected by intellectual property rights, including copyrights, trademarks and other proprietary rights, which rights are valid and protected in all media existing now or later developed, and contractually agree not to create derivative works based on the Information and not to use the Information for the purpose of enhancing competing works.

Course enrollees are granted a limited license to use, search, display, or print the Information contained on the institution's websites for their own personal non-commercial use only, provided the Information is not modified and a copy of this agreement is attached to any copies that are made. Any other use of the Information is strictly prohibited. None of the Information may be otherwise reproduced, republished or re-disseminated in any manner or form without the prior written consent from the institution.

All rights, including copyright, in any information which are linked to but not hosted on the Site continue to be owned by their respective owners.

Note that by using the institution's websites, you signify your agreement to this and future Copyright Notices. Your continued use of the institution's websites subsequent to changes to this Copyright Notice will mean that you accept the changes.

Copyright Law

Copyright is a form of legal protection provided by U.S. law, Title 17 U.S.C. §512(c) (2), which protects an owner’s right to control the reproduction, distribution, performance, display and transmission of a copyrighted work. The public, in turn, is provided with specific rights for fair use of copyrighted works. Copyrighted works protect original works of authorship and include

Specific information on copyright law and fair use may be found at the following sites:

Copyright Infringement

The copyright law provides the owner of a copyright the exclusive right to do the following:

The copyright law states, “Anyone who violates any of the exclusive rights of the copyright owner is an infringer of the copyright or right of the author.”

Generally, under the law, one who engages in any of these activities without obtaining the copyright owner’s permission may be liable for infringement.

Peer-to-Peer File Sharing

Peer-to-Peer (P2P) file sharing is a general term that describes software programs that allow computer users, utilizing the same P2P software, to connect with each other and directly access digital files from one another’s hard drives. Many copyrighted works may be stored in digital form, such as software, movies, videos, photographs, etc. Through P2P file sharing it has become increasingly easy to store and transfer these copyrighted works to others, thus increasing the risk that users of P2P software and file-sharing technology will infringe the copyright protections of content owners.

If P2P file-sharing applications are installed on your computer, you may be sharing someone else’s copyrighted materials without realizing you are doing so. As a user of any of the institution's networks, recognizing the legal requirements of the files that you may be sharing with others is important. You should be careful not to download and share copyrighted works with others.

The transfer and distribution of these works without authorization of the copyright holder is illegal and prohibited.

Violations and Penalties under Federal Law

In addition to Lionel University sanctions under its policies as more fully described below, anyone found liable for civil copyright infringement may be ordered to pay either actual damages or statutory damages affixed at not less than $750 and not more than $30,000 per work infringed. For willful infringement, a court may award up to $150,000 per work infringed. A court can, in its discretion, also assess costs and attorneys’ fees. For details, see Title 17, United States Code, Sections 504, 505.

Willful copyright infringement can also result in criminal penalties, including imprisonment of up to five years and fines of up to $250,000 per offense.

Lionel University Plans to Effectively Combat Unauthorized Distribution of Copyrighted Material; Student Sanctions

A student’s conduct in the University’s virtual classrooms and websites is subject to and must fully conform to the Student Code of Conduct policy and any other applicable Lionel University policies.

The University may monitor traffic or bandwidth on the networks utilizing information technology programs designed to detect and identify indicators of illegal P2P file-sharing activity. In addition to, or as an alternative, the University may employ other technical means to reduce or block illegal file sharing and other impermissible activities.

The institution will also provide for vigorous enforcement and remediation activities for those students identified through the University Digital Millennium Copyright Act policy as potential violators or infringers of copyright.

Disciplinary sanctions may be imposed on students identified as violators or infringers of copyright. Sanctions will be based on the seriousness of the situation and may include remediation based on a comprehensive system of graduated responses designed to curb illegal file sharing and copyright offenses through limiting and denial of network access or other appropriate means. These sanctions may be in conjunction with additional sanctions through the University’s Student Code of Conduct, or other University policy applicable to the particular situation.

Students who are subject to professional codes of conduct that apply to their enrollment at the University shall be sanctioned according to the requirements of the respective code.

Financial Aid consists of grants and loans provided by the federal government to those who can demonstrate eligibility. Each type of aid has specific eligibility requirements. Qualifying students may be eligible for more than one type of aid.

Generally, to be eligible for Federal Student Aid, a student must:

Demonstrate financial need (except for certain loans).

Have a high school diploma or a General Education Development (GED) certificate or state-specific equivalency credential, or complete a high school education in a home-school setting that is treated as such under state law.

Be enrolled or accepted for enrollment as a regular student working toward a degree or certificate in an eligible program.

Be a U.S. citizen or eligible noncitizens

Have a valid Social Security Number.

Maintain satisfactory academic progress once in school.

Not be in default on a federal student loan at any school or owe money on a federal student aid grant overpayment.

Certify that he or she will use Federal Student Aid only for educational purposes.

Be attending at least half-time (for loan program only).

Not have property subject to a judgment lien for any debt owed to the United States Government.

The student will need to complete a Free Application for Federal Student Aid (FAFSA) form in order to apply for Federal Student Aid. The form can be completed online at https://studentaid.gov/h/apply-for-aid/fafsa.

Lionel University's federal school code is: 042434

The student’s actual eligibility amounts will be determined from the information reported on the FAFSA.

Students are encouraged to reach out to the Office of Financial Aid or the Military office to determine if potential institutional financial aid assistance may be available to assist a student with extenuating circumstances.

Need-Based and Non-Need-Based Federal and State Financial Aid

Students are potentially eligible for a variety of aid programs; some are need-based and some are non-need based as determined by the information provided and verified on the FAFSA.

How Eligibility for Need-Based Aid is Determined and How Need-Based Aid is Awarded

Students are awarded financial aid based on the student’s financial need. Financial need is determined by a student’s Expected Family Contribution (EFC) (computed from information provided on the FAFSA) as compared to Lionel University’s Cost of Attendance (COA). Those who have a positive number remaining after the EFC is subtracted from the Cost of Attendance may qualify for some need-based aid sources. To meet with federal regulations, Lionel University defines the neediest students as those whose EFC = $0.

Resources Included in Financial Aid Packages are awarded as follows in this order:

1. The Pell Grant is awarded to students who meet the federal criteria as determined by EFC levels. The amounts of the award vary as the federal government determines.

2. Student Loans are awarded last. Students are offered their maximum loans based on dependency status (dependent or independent) and by level in college (first year or second year). Those who have completed less than 36 units at Lionel University are first-year students and those who have completed 36 units or more at Lionel University are second-year students.

Below are the programs Lionel University currently participates with:

Grants

Federal Pell Grants

The Pell Grant is aid that does not have to be repaid. Pell Grants are awarded to students who have a financial need as determined by the U.S. Department of Education standards. Annually, the U.S. Department of Education determines student eligibility for this Grant. For the 2023-24 award year, the maximum Pell Grant for a full-time student attending three quarters in the Award Year is $7395. Students eligible for a Pell Grant may qualify for less depending on their Estimated Family Contribution and enrollment status (number of credits taken) each quarter. Not all students will qualify for a Federal Pell Grant.

A student is eligible to receive a Pell Grant for up to 12 semesters or the equivalent. If a student has exceeded the 12-semester maximum, he or she will lose eligibility for additional Pell Grants. Equivalency is calculated by adding together the percentage of Pell eligibility that he or she received each year to determine whether the total amount exceeds 600%.

For example, if Mike’s maximum Pell Grant award amount for the 2022-2023 school year was $5,550, but he only received $2,775 because he was only enrolled for one semester, he would have used 50% of his maximum award for that year. If during the following school year (2023-2024), he were to enroll three-quarter time for the entire year, he will use 75% of his maximum award for that year. Together, he will have received 125% out of the total 600% lifetime limit.

Loans

Direct Loans are loans for students and parents to help pay for the cost of a student’s education after high school that tend to have less interest than alternative loans. The lender is the U.S. Department of Education, though the entity the borrower deals with, the loan servicer, can be a private business. The Borrower Rights and Responsibilities Statement issued by the Department of Education with the Master Promissory Note includes information regarding use of the loan money, information the borrower must report to the Department of Education after the loan is received, the amount the borrower may borrow, the interest rate, payment of interest, the loan fee, repayment incentive programs, disbursement information, loan cancellation, the grace period, loan repayment information, late charges and collection costs, demand for immediate repayment, defaulting on the loan, consumer reporting agency notification, deferment and forbearance options, discharge, loan consolidation, Department of Defense and other federal agency loan repayment, and Americorps program education awards.

A Disclosure Statement is issued to the borrower by the Department of Education once the Department receives a loan origination record from the school. A Notice of Disbursement(s) Made Letter is issued to the borrower by the Department of Education once the Department receives a disbursement that was made to the borrower.

Federal student loans are required by law to provide a range of flexible repayment options, including, but not limited to, income-based repayment, income-contingent repayment plans, and loan forgiveness benefits, which other student loans are not required to provide. Federal Direct Stafford loans are available to students regardless of income. Before taking out loans, students should visit the Department of Education’s Federal Student Aid website at https://studentaid.gov/understand-aid/types/loans to learn more.

Subsidized Federal Direct Loan

The Subsidized Federal Direct Loan program provides low-interest loans through the U.S. Department of Education’s Direct Loan Program. It is awarded on the basis of need and tends to have less interest than private loans. The maximum annual loan amount for undergraduate students is $3,500 for the first academic year, and $4500 for the second academic year, and $5,500 for the third and fourth academic years. In addition, the Department of Education will remove origination and other fees (if applicable). Beginning July 1, 2012, only undergraduate students are eligible for subsidized loan funding. The Federal government pays the interest while the student is in school, in grace, and during deferment periods. Effective for loans disbursed on or after July 1, 2012, interest begins accruing on these loans when the student graduates or drops below half-time enrollment status. Repayment begins six months after the borrower ceases to be enrolled at least half-time. The minimum repayment amount is $50 per month, but it may be greater depending on the amount borrowed.

However, subsidized Federal Direct loans provide many flexible repayment plans as outlined in the loan counseling materials. Payments are based on the repayment plan selected by the student. Current interest rates can be found at the Department of Education's Federal Student Aid website at https://studentaid.gov/understand-aid/types/loans.

Borrowers with other outstanding loans may be able to consolidate eligible loans and make only one monthly payment. Please refer to the loan entrance counseling materials found at https://studentaid.gov/app/launchConsolidation.action for additional information.

Unsubsidized Federal Direct Loan

Unsubsidized Student Loans are federally guaranteed loans that are available for students who desire to pursue education, but lack the financial resources to do so. These loans are not based on financial need. Interest on the unsubsidized student loans starts to accrue as soon as the loan is disbursed to the school. The federal government does not pay the interest on the loan while the student is in school. These are fixed interest loans and a student is not required to start making repayments while he or she is in school. Students are not required to make interest or principal payments until 6 months after graduation or dropping below half-time. These loans can be used to pay for the total expenses of your education: tuition, housing, reading materials, and other expenses related to studies.

https://studentaid.gov/understand-aid/types/loans

Student loan borrowers are responsible for all interest that accrues on the loan while in school, in grace, and during deferment periods. The student may elect to make interest payments while in school to avoid the capitalization of interest and to lower the overall repayment debt. Loan repayment will begin six months after the student leaves school or attends less than half time.

The interest rate for undergraduate unsubsidized loans can be found at https://studentaid.gov/understand-aid/types/loans.

Please see the Financial Aid Administrator at the school to receive further information regarding the maximum Unsubsidized Federal Direct annual loan amounts for the second or subsequent academic years.

All federal loans will be reported to the U.S. Department of Education’s National Student Loan Data System (NSLDS) as part of the student’s financial aid history. The information will be accessible to authorized agencies, other post-secondary institutions, lender and Federal loan servicing agencies.

Lionel University does participate in the PLUS Loan program. Students are encouraged to contact the Lionel Financial Aid Team at 800-650-4772 x3 or financial-aid@lionel.edu, to review the PLUS loan option.

State Aid Programs

If you were in Foster Care prior to reaching the age of 18 in California, please access the following resource:

https://mygrantinfo.csac.ca.gov/Help/FosterYouth.asp

Lionel University does not currently participate in the Cal Grant program for California residents.

Please refer to the following website to determine if there are any other forms of California State Aid apply to you:

http://www.csac.ca.gov/doc.asp?id=33

If you believe you qualify for other forms of funding through California or your state of residency, please refer to the particular agency providing the aid to inquire about requirements, and contact the Financial Aid Office to include it in your financial aid package.

The U.S. Department of Education’s Office for Civil Rights (OCR) enforces, among other statutes, Title IX of the Education Amendments of 1972, Title IX protects people from discrimination based on sex in education programs or activities that receive Federal financial assistance. Lionel University is committed to providing a work and school environment free of unlawful harassment or discrimination.

Title IX Coordinator:Lionel University ensures that its employee(s) designated to serve as Title IX Coordinator(s) have adequate training on what constitutes sexual harassment, including sexual violence, and that they understand how the institution’s grievance procedures operate. Because complaints can also be filed with an employee’s supervisor or Human Resources, These employees also receive training on the institution’s grievance procedures and any other procedures used for investigating reports of sexual harassment.

TITLE IX POLICY

Lionel University is committed to providing a work and school environment free of unlawful harassment or discrimination. In accordance with Title IX of the Education Amendments of 1972, Lionel University prohibits discrimination based on sex, which includes sexual harassment and sexual violence, and Lionel University has jurisdiction over Title IX complaints which should be directed to the Title IX Coordinator. Employees of Lionel University are required to take our mandatory Sexual Harassment and Prevention Training upon hire and every two years thereafter. Lionel University policy prohibits harassment or discrimination based on race, religion, creed, color, national origin, ancestry, sex (including pregnancy, childbirth or related medical conditions), military or veteran status, physical or mental disability, medical condition, marital status, age, sexual orientation, gender, gender identity or expression, genetic information or any other basis protected by the federal, state or local law.

Lionel University TITLE IX and anti-harassment policy applies to all persons involved in the operation of the institution, and prohibits unlawful harassment by any employee of the institution, as well as students, customers, vendors or anyone who does business with the institution. It further extends to prohibit unlawful harassment by or against students. Any employee, student or contract worker who violates this policy will be subject to disciplinary action. To the extent a customer, vendor or other person with whom the institution does business engages in unlawful harassment or discrimination, the institution will take appropriate corrective action.

As part of the institution’s commitment to providing a harassment-free working and learning environment, this policy shall be disseminated to the institution’s community through publications, the school website, new employee orientations, student orientations, and other appropriate channels of communication. Lionel University provides training to key staff members to enable the institution to handle any allegations of sexual harassment or sexual violence promptly and effectively. Lionel University will respond quickly to all reports, and will take appropriate action to prevent, to correct, and if necessary, to discipline behavior that violates this policy.

TITLE IX Definitions

Sexual Harassment

Is defined as unwelcome is defined as unwelcome advances, requests for sexual favors, other verbal or physical sexual conduct, or any other offensive unequal treatment of an employee, student, or group of employees or students that would not occur except for their sex when:

Sexual Harassment is a violation of Section 703 of Title VII of the Civil Rights Act of 1964 as amended in 1972, (42 U.S.C. S2000e, et. seq.), and Title IX of the Education Amendments of 1972 (20 U.S.C. 1691, et. seq.), including the Clery Act and the Violence Against Women Act (VAWA) and is punishable under both federal and state laws. Forms of sexual harassment include, but are not limited to, sexist remarks or behavior, constant offensive joking, sexual looks or advances, repeated requests for dates, unwelcome touching, promise of reward for sexual favors. Students, faculty or staff who experience sexual harassment are encouraged to make it clear to the alleged offender that such behavior is offensive. However, failure to comply with this provision does not defeat the investigation. Includes quid pro quo harassment perpetuated by an educational institution’s employee; and all other forms of sexual harassment, where the conduct is “so severe, pervasive, and objectively offensive” that it denies the victim equal access to education, as set forth by the Supreme Court in Davis v. Monroe County Board of Education.

Sexual Violence

Means physical sexual acts perpetrated against a person’s will or where a person is incapable of giving consent. A number of acts fall into the category, including sexual assault or harassment based on sexual orientation, domestic violence, dating violence, and stalking. Alleged sexual violence against another may also constitute a crime resulting in an additional, independent law enforcement investigation falling outside of this Grievance Policy. These acts will not be tolerated at Lionel University as such acts are inappropriate and create an environment contrary to the goals and mission of Lionel University. Any such acts will be thoroughly investigated and will subject an individual to appropriate disciplinary sanctions and/or possible action by appropriate law enforcement agencies.

Sexual Assault

Includes rape, acquaintance rape, fondling, incest, and statutory rape, as well as other forms of non-consensual sexual activity.

Domestic Violence

Means a felony or misdemeanor crime of violence committed by a current or former spouse or intimate partner of the victim, a person with whom the victim shares a child in common, a person who is co-habitating with or has co-habitated with the victim as a spouse or intimate partner, a person similarly situated to a spouse of the victim under domestic or family violence laws of the jurisdiction in which the crime of violence occurred, or any other person against an adult or youth victim who is protected from that person’s act under the domestic or family violence laws of the jurisdiction in which the crime of violence occurred.

Dating Violence

Means a violence act committed by a person who is or has been in a social relationship of a romantic or intimate nature with the victim and where the existence of such a relationship shall be determined based on the reporting party’s statement and with consideration of the following factors: the length of the relationship, the type of relationship, and the frequency of interaction between the persons involved in the relationship. Dating violence includes, but is not limited to, sexual or physical abuse or threat of such abuse and dating violence does not include acts covered under the definition of domestic violence.

Stalking